Quant Trading vs Systematic Trading

A recurring confusion in conversations

This question comes up all the time in conversations and with practitioners:

What does quant trading actually mean?

And is it the same as systematic trading?

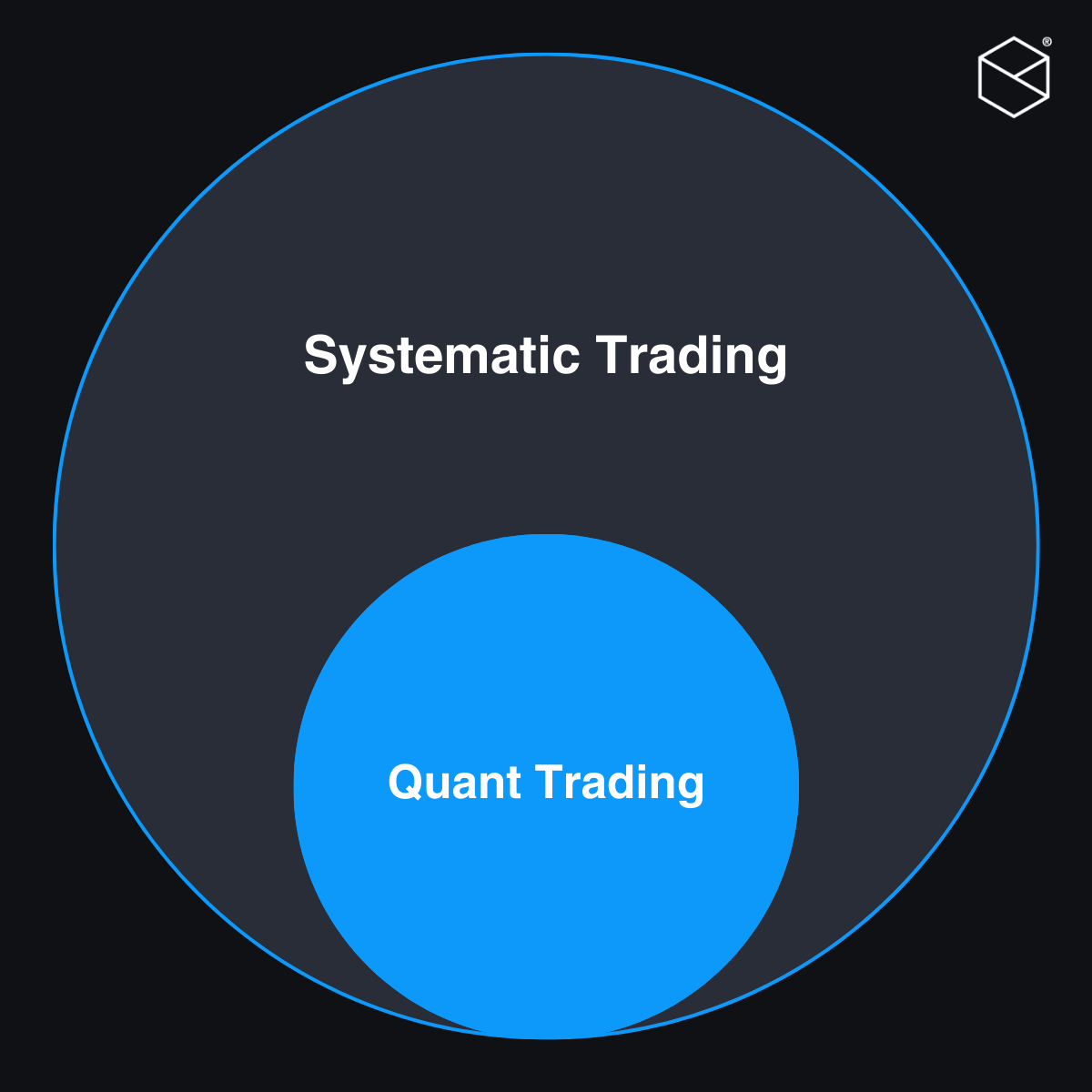

Here’s a clear distinction.

What Systematic Trading Means

Systematic trading means making trading decisions based on predefined rules, executed consistently, rather than on gut feel or discretionary judgment.

It’s about discipline and repeatability.

A systematic trader eliminates emotion out of execution and ensures that decisions follow a process that can be replicated and evaluated.

What Quant Trading Means

Quant trading is, at its core, systematic trading powered by data, models, and rules.

It means making decisions using:

Data

Mathematical models

Statistical reasoning

Algorithmic rules

In practice, quant trading usually includes:

• A hypothesis (e.g. trends persist, cheap assets outperform)

• Measurable signals (momentum, valuation, macro, alt data)

• Statistical testing and validation

• Portfolio construction (sizing, constraints, diversification)

• Risk modeling (vol targeting, drawdown control, hedging)

• Often automation (backtesting, execution, monitoring)

Examples of Quant Trading

To make this less abstract, quant trading includes:

• Factor trading (value, momentum, quality, low vol)

• Statistical arbitrage (pairs trading, mean reversion)

• Trend following / CTA-style systems

• Volatility and options strategies

• Market making

• ML-driven strategies (careful: often overhyped)

• Carry / term structure (rates, FX, futures, vol carry)

• Risk premia / style premia (institutional framing of factors)

• Liquidity / microstructure signals

• Event-driven quant (earnings drift, announcement effects, flows)

What Quant Trading Is Not

Quant trading is not necessarily:

• “AI trading”

• High-frequency

• Complex

• Guaranteed to beat the market

These are often misconceptions. The defining characteristic is not hype or speed. It is rigorous, model-driven decision logic.

When Does Systematic Become Quant?

A systematic strategy becomes quant when its rules are derived from statistical research and model-based decision logic, not just fixed heuristics.

You’ve crossed into quant territory when you introduce:

Statistical validation of signals

Cross-sectional ranking or factor modeling

Explicit risk modeling

Portfolio optimization under constraints

Signal combination based on quantitative weighting

Parameter estimation grounded in data rather than convention

In Short

Systematic = rule-based execution.

Quant = research-driven modeling that determines the rules.

The difference is not automation.

It’s the depth of statistical reasoning behind the rules.